DEERFIELD BEACH, Fla. (PRWEB) May 5, 2007

DEERFIELD BEACH, Fla. (PRWEB) May 5, 2007

Grand Rapids, MI (PRWEB) March 23, 2009

Grand Rapids, MI — Despite the rough financial occasions and record foreclosure numbers, there has never ever been a far better time to get and invest in genuine estate. But this new actual estate marketplace has brought new guidelines, and with it a host of new dangers for those who enter ill-prepared.

“Even though there are undoubtedly individuals hurting out there, banks and mortgage lenders are seeking to make bargains any way they can,” stated Chip Cummings, 27-year business professional and ideal-promoting author. “With the new guidelines for short sales and loan modifications, the possibilities out there for investors and even first-time homebuyers are the very best we’ve seen in decades. But you have to know what to appear for, and much more importantly, what to ask for.”

Dabbling in the true estate foreclosure and the quick sale industry is not for the faint of heart. Such are the lessons in Cummings’ new release “Cashing In on Pre-foreclosures and Short Sales – A True Estate Investors Guide to Creating a Fortune, Even in a Down Marketplace” (Wiley). In this his sixth book, Cummings teaches readers how to effectively evaluate both the potential and the dangers involved with a foreclosure house, and reveals a particular 17-step strategy for negotiating short sales, loan modifications and sales agreements that result in win-win transactions for sellers and mortgage lenders – as properly as the buyer.

The book comes total with updated foreclosure suggestions and dozens of prepared to use letters, forms, worksheets, agreements and checklists to support both genuine estate pros and novices alike navigate the occasionally muddy and turbulent waters of the foreclosure and quick sale process. Tapping into a vast network of real estate and organization professionals, Cummings also shares a wide range of downloadable resources for those hunting to construct wealth for the duration of these difficult financial times.

Access to these downloads, as properly as electronic copies of all the foreclosure, quick sale and loan modification types and letters can be identified at the “Foreclosure & Quick Sale Resource Download” Web page

“Cashing In on Pre-foreclosures and Short Sales” is now available in bookstores nationwide or on the web by way of Amazon, Barnes & Noble and other retailers. Author Chip Cummings has appeared on main networks such as FOX, NBC and ABC and is accessible for interviews or appearances upon request. A media kit is offered at “Chip Cummings Media Area”, or by calling Northwind at (866) 977-7900.

###

Ithaca, NY (PRWEB) June 30, 2013

GIVE Leadership Institute co-founder Al Gonzalez hosted a distinguished line-up of guests during the first month of his weekly WebTallkRadio.net show, Major Beyond the Status Quo, touching on an array of essential concepts at the heart of concerns that influence leaders and their teams such as negativity bias, sustainable leadership such as employee engagement, workplace bullying and the Triple Bottom Line of Individuals, Profit and Planet.

Bob Burg, co-author of the ideal selling book The Go-Giver, shared his thoughts on how his 5 Laws of Stratospheric Success aid to enhance the high quality of leadership and provide sustainable accomplishment in a show titled, Are You a Go-Giver, a Go-Getter, or a Go-Taker?

Gonzalez cited Burg as a believed leader, a master of the sales procedure and one of (his) all-time heroes in the location of leadership improvement. He explained that reading The Go-Giver really inspired the name of his institute. Your book was a confirmation that you can lead differently and be courageous and that you just have to uncover a balance.

Burg responded by explaining that the key idea of the Go-Giver is shifting ones focus from acquiring to providing, and in this context, that implies constantly and regularly supplying worth to other folks.

Deborah Mann from the Charles H. Dyson College of Applied Economics and Management at Cornell University was interviewed for Why Do CEOs Fail?, a show that integrated a discussion of a leadership tool recognized as 5 Practices of Exemplary Leadership, a framework that can assist anybody perfect the art of leadership.

From her viewpoint as the lead coordinator and the administrator of the leadership portion of the of the BOLD (Enterprise Opportunities in Leadership and Diversity) system at the Dyson College, Mann feels the tool is ideal for any leader as nicely as the BOLD students. I like this model because it is about leadership being everybodys enterprise, not about a title or position. Everybody is capable of performing it, they just require to recognize leadership behaviors and then articulate them.

In three Filters for Employee Engagement, Maya Mathias, author of How To Innovate: Unleash Your InnoMojo, discussed how leaders want to realize and relate to their teams more closely if they actually want to succeed in the new international marketplace.

Ever given that the dawn of the Industrial Age, we have, as a society, an economy and a market location, truly valued and to some extent overvalued the contribution of the left brain – process, routine, repetition, efficiency and we have rewarded those items a lot more than time. Now we are moving to much more of a inventive or conceptual economy, and being inventive calls for a ton much more empathy.

Mathias cited this as a key to innovation as properly as employee engagement. If you cant have that level of empathy, you cant produce one thing distinct or deign something that meets your consumers needs, due to the fact you cant even empathize with your buyers. As leaders, we are taught to turn off empathy when we walk into the workplace and we want to understand as leaders that our coworkers and employees and our staff members want some of that empathy, too.

Leadership Lessons from At Danger Youth featured a conversation with Annie Socci, Wilderness Instructor with Outward Bound, who spoke about how her work with young folks demonstrates that building a culture of trust exactly where folks can use their inventive freedom to consistently exceed expectations depends on clear expectations from leaders and group members.

With our at-threat youth and in the organization planet, the trifecta of expectation, communication and constant action function hand in hand to decide how considerably trust there is going to be, and how wholesome your partnership is going to be.

Jim Volkhausen, Assistant Director of the Cornell Team and Leadership Center joined Gonzlez for Is Team Creating a Waste of Time and Income? a show exploring the significance of team constructing and how to make certain the investment final results in a transformative experience for the team.

When asked for his thoughts on the all-also-common view that group developing is a waste of time and money as it takes staff away from production (despite the over $ 350 Billion dollars that research say is lost in productivity because of disengaged personnel), Volkhausen mentioned that my experience functioning with groups is that taking the time to really support develop unity within an organization and develop a sense of engagement is crucial in moving towards accomplishment.

Fairfax, VA (PRWEB) October 21, 2008

A new cost-free report at Mortgage Loan Modifications for Profit shows how to earn a profit doing loan modifications for homeowners.

“At least 3 million homeowners want loan modifications,” stated Richard Geller, developer of the free report. “These home owners do not have the negotiating capabilities, the expertise or the persistence necessary to get the loan mods completed.”

According to Mr. Geller, most home owners wait until the last minute ahead of applying for a mortgage loan modification. “And then they never know how to go about it,” Geller stated.

There is a lot to performing loan mods and most property owners are lost, according to Geller. “That is why we offer you this cost-free report. We show you how you can do loan modifications not just for your personal mortgage, but for other people, and hopefully earn a profit undertaking so.”

Geller mentioned the demand is quite higher. “I have individuals calling and emailing me continually. Most of them never want foreclosure. They want to remain in their residence. They are asking for aid in receiving a loan modification.”

Fees for performing loan modifications differ, Geller said. But frequently they are equal to 1 mortgage payment that the homeowner must be making. “So if they have been paying $ 1,500 per month on their mortgage payment, their fee might be $ 1,500,” Geller explained. “But that’s up to the business owner who is in the loan mod organization. The entrepreneur determines how much to charge.”

In some states, laws have been passed that regulate how you can strategy a homeowner about avoiding foreclosure. Geller explained,”these laws in common prohibit prepayment for services. So the report that you can do loan mods and not gather something till you have performed the service for the homeowner.”

Geller said that loan mods for profit is potentially excellent for a mortgage broker, a true estate agent, or a home investor who desires to assist themselves and support others. “There is enormous demand,” Geller said, “and if you are a loan officer or an agent, you want to be where the demand is. That is in loss mitigation right now, not in new loans.”

To get the cost-free report, merely pay a visit to Mortgage Loan Modifications Unique Report.

###

Uncover More Loan Modification Services Press Releases

Hidden Hills, CA (Vocus/PRWEB) February 01, 2011

The recent report by the federal commission on the economic crisis clearly demonstrates how government is allowing banks to evade duty for the crisis and helping banks far more than citizens, according to Mitchell J. Stein, Esq., of MJS Associates.

“As an alternative of serving the interests of the people, this commission and its meaningless report have completed absolutely nothing far more than serve the banks and institutions like Fannie Mae and Freddie Mac that are responsible for producing the issue:, stated Mitchell J. Stein, Esq., a 25-year award-winning litigator, trial lawyer, financier, and entrepreneur who has represented numerous of the worlds largest companies and has been involved in some of the highest profile circumstances in the Nations history.

Rather than supply the bipartisan view of the origins of the monetary crisis mandated by Congress, the panel split along partisan lines and released three competing assessments. The report was released simultaneously with two dissenting reports from the Republican minority. The majority report blamed a range of culprits for the economic crisis from overextended home owners to reckless executives and timid regulators, the minority reports on international variables and government intervention into the housing marketplace.

According to Mitchell J. Stein, Esq., the majority reports conclusions had been vague and meaningless, including findings that human beings, not other elements like nature or technology, have been accountable for the crisis, action and inaction by these human beings was the lead to of the crisis and that the crisis could have been avoided.

This report is a flimsy attempt by Washington insiders and bankers to keep away from blame and evade duty for the mess they have produced, stated Mitchell J. Stein, Esq. The majority reports conclusions are meaningless and utterly useless.

The report includes particulars from more than 700 interviews conducted during an 18-month investigation seeking to clarify the housing bubble that ended badly, triggering a international credit crisis and the worst recession in decades. Media coverage integrated details about the interviews, including those with leaders of investment bank Goldman Sachs Group Inc., government regulators, particularly present and former officials at the Federal Reserve, and executives such as former Countrywide Financial Corp. Chief Executive Angelo R. Mozilo, who final year agreed to spend a record $ 22.five-million fine to settle a government fraud lawsuit over the lender’s near-collapse. Coverage of the report in the Los Angeles Occasions also indicated that Mozilo told the panel he got swept up in a “gold rush” mentality that had taken over the nation.

It is outrageous that the Commissioners permitted Mr. Mozilo to pass the blame onto citizens without having clearly identifying the leading injurious role he and Countrywide played in damaging our economy and hurting millions of home owners, mentioned Mitchell J. Stein, Esq.

According to the Los Angeles Instances, the majority report concluded that “a crisis of this magnitude can’t be the function of a handful of bad actors” and ascribed duty to each organizations and people in company and the government.

We agree with the minority reports that blame ought to be focused on intervention in the housing industry including assistance for Fannie Mae and Freddie Mac and that this report was part of a partisan approach created to make predetermined final results, so its conclusions are inconsequential said Mitchell J. Stein, Esq. It is ironic that soon after all the pain inflicted on our citizens by the economic meltdown, this commission’s investigation and report is just yet another instance of Washington waste.

According to Mitchell J. Stein, Esq., there is constantly a silver lining to the black cloud. “For a lot more than two years for the duration of this meltdown, my mantra has been distinct that I by no means expected the federal government to take duty. I in no way anticipated the banks to take responsibility, although I need to admit after the government doled out the first trillion dollars of TARP funds I believed — if only for a second — that aid was on the way. Then I woke up from my a single-second dream into the nightmare of dealing with criminals, liars and persons forging documents. Having represented these very same banks and their governmental partners for years, I was and am unwilling to enable my customers to turn out to be an additional statistical imbecile who goes by way of the Bank drill of submitting economic info to the bank and then resubmitting it and then resubmitting it and then resubmitting it and then resubmitting it. I have never ever carried out, and nor shall I now do, ‘loan modifications’ simply because that is a term created up by banks to get time until the wave of public sentiment against banks has subsided. So what is the very good news, asked the Doberman? Nicely get ’em in Court,” stated Mitchell J. Stein, Esq.

ABOUT MITCHELL J. STEIN & ASSOCIATES

Mitchell J. Stein & Associates is a California-primarily based law firm founded by M.J. Stein, Esq. a 25-year award-winning litigator, trial lawyer, financier, and entrepreneur who has represented a lot of of the worlds biggest companies and has been involved in some of the highest profile situations in the Nations history. The Firms philosophy is primarily based on the belief that their clientele demands are of the utmost importance and, as a outcome, a higher percentage of the Firms business has been from repeat consumers and referrals. The Firms practice areas include Complex Litigation, Bank Problems, Mergers & Acquisitions, Industrial and Residential Foreclosures , and Bankruptcy Litigation. Mr. Stein is also the founder of VIPS Foundation (Victims of Injustice Discomfort and Suffering), via which victims nationwide, over the final 15-years, have received help following unfortunate events that subjected them to oppression or mistreatment. In that regard, Mr. Stein received the inaugural Mitchell J. Stein Benefactor Award from the National Organization for Victims Assistance (NOVA) for his perform in guarding victims rights. Go to http://www.mjsteinassociates.com or http://www.dobielaw.org for a lot more info.

###

Sarasota & Manatee, FL (PRWEB) November 01, 2011

Nationally recognized genuine estate professional, John Michailidis, offers totally free seminar for FL home owners behind on mortgage payments. The unemployed, underemployed, divorced, and those who’ve seasoned recent health-related emergencies are being targeted for Foreclosure. Now, Sarasota & Manatee county residents can discover how to beat Foreclosure thru a “Brief Sale With Complete Deficiency Waiver” even when they owe a lot far more than the property’s worth. Ideas on how to virtually assure approval even if prior Quick Sale attempts have failed will be provided.

Sarasota & Manatee county Florida home owners behind on their mortgage payments and who are either unemployed, underemployed, divorced, or who have experienced recent health-related misfortunes are being targeted.

According to national genuine estate professional, John Michailidis, the menace is foreclosure, and by some estimates upwards of 40% of Sarasota and Manatee homeowners are vulnerable. A cost-free report outlining the dilemma can be downloaded at http://NoEquityHomeSaleReport.com.

“Foreclosure destroys families and communities, and has literally displaced millions of American citizens,” said real estate specialist John Michailidis, GRI, CRS, JD. “The dirty small secret that bankers and politicians look to be ignoring is the truth that Foreclosure is practically one hundred% avoidable thru the use of a Brief Sale With Deficiency Waiver.”

With congressional watchdogs testifying that the record of government loan modification applications, “has been nothing short of abysmal,” many delinquent homeowners are below the false assumption that Foreclosure is unavoidable.

According to Mr. Michailidis, “A foreclosure most undoubtedly is avoidable and I’ve got the track-record to prove it. In practically each case we’ve taken on, we have been in a position to safe a Short Sale with Full Deficiency Waiver, which means the homeowner was able to move on with their life, totally free from mortgage debt, and with out the specter of the banks coming after them down the road.”

Mr. Michailidis is presenting a series of cost-free, on the internet, community-outreach public seminars for Sarasota and Manatee County Florida home owners who are behind on their mortgages and worried about foreclosure. “The goal of these free seminars is to disseminate as widely as achievable information that is getting suppressed by the banks. Participants will be capable to submit queries by way of email throughout the event and obtain customized responses,” he said. Scheduling and registration details is offered at http://FloridaForeclosureEnders.com.

Mr. Michailidis is a recognized genuine estate author and speaker, and the broker/owner of SaraMana Properties, exactly where he focuses his company on exclusively helping homeowners to keep away from foreclosure by means of Quick Sales. He is also a graduate of the Northwestern University School of Law in Chicago and is a member of the Illinois Bar. A message can be left for Mr. Michailidis at 941-548-7771, or by way of e mail at info(a)SaraManaProperties.com.

###

Calabasas, CA (PRWEB) June 22, 2011

Lead lawyer at for the Law Offices of Kramer and Kaslow, Philip Kramer, not too long ago released comments on the newest Mortgage Litigation Index numbers compiled by MortgageDaily.com. According to the newest Mortgage Litigation Index, mortgage servicing litigation increased 88 percent for the duration of the first quarter, according to MortgageDaily.com. The increasing quantity of lawsuits suggests economic institutions will be increasingly below pressure to resolve outstanding mortgage and foreclosure problems.

Philip A. Kramer, a noted lawyer who represents hundreds of property owners who have filed consolidated plaintiff litigation lawsuits against six of the nations largest lenders, commented on what he feels that the statistics indicate.

What youre seeing here are the cumulative final results of years of egregious conduct that have not been properly addressed by regulatory authorities. Kramer finds especially noteworthy the dramatic increase in investor and criminal litigation. If you appear at these charts, says attorney Kramer, You see that investors are increasingly turning to the courts for redress. The courts have turn out to be the significant avenue of redress due to the fact other institutions have failed. At least until now. The charts also show an elevated number of criminal suits which suggests that government neighborhood, state and federal — is developing increasingly active in redressing some of these troubles.

Philip Kramer observes, It looks to me like we have reached a tipping point. Either banks are going to settle voluntarily, or the courts are going to impose options. A single way or another, it appears like a resolution is on the way.

A lot more of Philip Kramers thoughts can be located at the Kramer and Kaslow weblog.

ABOUT PHILIP KRAMER

PHILIP A. KRAMER is the senior partner of the Law Office of Kramer & Kaslow, in Calabasas, California. Kramer & Kaslow is Martindale Hubbell AV rated. Mr. Kramer is a perennial recipient of the prestigious Southern California Super Lawyer award.

Mr. Kramer received his undergraduate degree from Ohio State University and his Juris Doctorate from the Catholic University of America, in Washington, DC. His practice emphasizes industrial litigation and trial advocacy, with a concentration on organization litigation, and genuine property matters. He has prosecuted and defended cases for over twenty five years.

Mr. Kramer is a licensed real estate broker and has spent considerable time providing legal services in connection with genuine estate concerns relating to loan modification and loss mitigation, land use and zoning, environmental problems, easements, building and improvement, finance, and landlord tenant matters.

Mr. Kramer is admitted to practice before all courts in the State of California, the United States Supreme Court and the United States Court of Military Appeals. Mr. Kramer has tried in excess of 200 instances. He has appeared on nationally televised programs concerning pre-trial process and trial strategy and has appeared as a guest lecturer on topics ranging from constitutional law to trial practice, and Mr. Kramer frequently lectures on a broad spectrum of numerous legal and company concerns.

Mr. Kramer also serves as a Judge Pro Tem for the Los Angeles Superior Court and as a Mediator.

Mr. Kramer is also a previous president of the Los Angeles West Inns of Court, a national organization committed to bringing professionalism and civility back into the legal profession. He also serves on quite a few Boards of Directors and serves as an officer in several companies. For much more info get in touch with (818) 224-3900 or check out http://kramer-kaslow.com

###

Minneapolis, MN (PRWEB) August 07, 2012

On August 3,2012, The U.S. Division of Housing and Urban Development (HUD) and the U.S. Department of the Treasury released the July edition of the White Home Housing Scorecard a complete report on the nations housing market place. Data in the Housing Scorecard shows continued indicators of recovery as foreclosure begins and completions declined in June.

The report additional says, ‘In addition, the inventory of homes for sale remained low at existing pace, it would take six.6 months to sell the provide of existing homes on the market and four.9 months to clear the new properties on the market place. Authorities contemplate a six month supply of homes to be a balanced industry. Distressed sales stay a key issue, even so, as the effect of significant delinquencies and underwater mortgages continue to temper market gains”.

“The Residence Cost-effective Refinance Plan (HARP) continues to offer the deepest and most sustainable help offered to avoid foreclosure. Home owners in the program have a high likelihood of effectively overcoming their financial hardship and keeping their mortgage payments for the long term, mentioned Treasury Assistant Secretary for Financial Stability Tim Massad. We remain committed to using the tools we have obtainable to aid our country heal quicker from an unprecedented crisis.

HUD’s report gives specifics on how homeowners in HAMP continue to demonstrate extended-term good results in the program. Tabulated stats from the end of June show:

far more than 1 million property owners have received a permanent HAMP modification

individually saving roughly $ 537 on monthly mortgage payments

savings on a national level total $ 13.9 billion

75% of homeowners with non-GSE mortgages benefited from principal reduction with their HAMP modification

distressed property sales accounted for 24% of all re-sales in May possibly, down from a revised 26 % in March and down from 29% the preceding year

86% percent of property owners starting the plan in the final two years have received a permanent modification

The report points to HAMP modifications extended-term achievement by stating that they “continue to exhibit lower delinquency and re-default prices than private business modifications, with 94 percent of homeowners nonetheless current on their modified payments soon after six months”.

Property Location interrupts DeMarco’s recent letter to Congress to mean that he believes HAMP’s extended-term successes is at threat.

DeMarco’s has remained powerful in his leadership of Fannie Mae and Freddie Mac funds, standing at odds with The Treasury Division. He believes proposing a broad sweep of mortgage principal reductions would have damaging influence on mortgage markets. He stated, “Longer-term, this view could lead to larger mortgage rates, a constriction in mortgage credit lending or both, outcomes that would be inconsistent with FHFAs mandate to promote stability and liquidity in mortgage markets and access to mortgage credit”.

This months indicators show momentum not noticed because ahead of the housing crisis as refinances via our enhanced Residence Reasonably priced Refinance Program continue to surge – HARP loans represented 20 % of total refinance volume in Might, the biggest improve given that the plan was launched in 2009,” said HUD Acting Assistant Secretary Erika Poethig. He continued, “But with so a lot of households nevertheless struggling to make ends meet, its clear that we have a lot more function ahead,”

As the scorecard validates HARP is attaining sustainable mortgage reductions for property owners, Jenna Thuening, owner of Residence Location, hopes this encourages other people to participate in the plan and request an Independent Foreclosure Overview if their home is underwater.

Extended Term Guidance from mortgagenewsdaily.com states they “continue to advocate against trying to ‘get ahead’ of current marketplace movements due to the high degree of uncertainty. In the past, we would have interpreted that suggestions as a suggestion to lock, but in the recently ‘low and sideways’ environment, it is possibly better-read as a suggestion to go with the flow of steadily decrease prices until we see the pattern definitively break.”

Minneapolis and St. Paul region home owners might get in touch with Home Destination if needing a mortgage reduction or are facing foreclosure at 612-396-7832.

Uncover Far more Loan Modification Press Releases

Chicago, IL (PRWEB) June 09, 2013

While The Federal Savings Bank is busy with some veterans trying to make new property purchases, other veterans are kickstarting little businesses – an endeavor the Tiny Business Administration would like to assistance.

The SBA plans to increase its lending to veterans by $ 475 million more than the next five years, adding an additional 2,000 veterans expanding or starting their personal tiny company. According to the SBA, 9 % of veterans are tiny organization owners. Despite two.45 million veteran-owned firms employing more than 5 million individuals, the SBA notes that they nevertheless struggle to secure adequate financing via traditional channels.

A important pledge to substantial people

The 5 % increase to veteran lending is referred to as the Veteran Pledge Initiative, and will certainly help the more than 21.five million veterans in the U.S. transition to the civilian workforce and develop jobs.

“Our service males and girls have created incalculable contributions and sacrifices for our country, and supporting them as they pursue their dreams to begin or develop their own company is one of SBA’s highest priorities,” said Karen Mills, SBA administrator. “Through this partnership with national and regional and neighborhood lending partners, we stand ready to serve veteran entrepreneurs with loan guarantees, entrepreneurial instruction, and crucial tools to help them start off companies, drive the nearby economy and produce jobs for themselves and their communities.”

In order to make this pledge reality, the SBA has formed lending partnerships with 20 massive financial institutions as well as hundreds of community banks scattered throughout the U.S. The program will be implemented alongside the VetLoan Advantage plan that offers instruction and discounted financing to veteran organization owners. In addition, there are 15 Veterans Organization Outreach Centers with thousands of integrated tiny company development centers with even a lot more little organization counselor volunteers that help a lot more than 200,000 reservists, veterans and disabled servicemen, according to FOX Enterprise.

“This new SBA initiative really highlights the Administrations’ commitment to assisting the nations’ veterans,” said Terry Robinson, president of Sunovis Financial. “It is ironic that even even though our nations’ veterans are willing to threat their lives, a lot of lenders are unwilling to risk lending to veterans. I locate the program to be an superb modify to this mindset.”

Contact Federal Savings Bank, a veteran-owned bank, at (877) 788-3520 if you are a veteran interested in beginning your own company and need financing assistance.

Chicago, IL (PRWEB) July 16, 2012

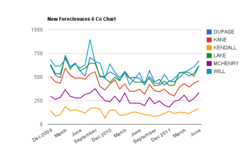

According to stats compiled by ILFLS.com, the Illinois Foreclosure Listing Service, Chicagoland foreclosures are still on the rise for June 2012 in the following six counties: Will, Kane, Lake, McHenry, Kendall, and DuPage. According to the information, house foreclosures have enhanced overall in the Chicagoland region compared to the earlier month, May possibly 2012, and compared to final year, June 2011.

In June, six of the seven Chicagoland counties showed an increase in foreclosure activity compared to May possibly 2012. The total quantity of property foreclosure filings for the seven counties for May possibly 2012 was six,440. This is moderately reduce than the total for June which reached six,645. This is an general enhance of a small over three% compared to final month. The largest increases from May to June had been seen in the counties of McHenry, Lake, and Kendall. The biggest enhance was observed in McHenry going from 273 in May possibly and improved over 23% to 336 in June. Lake county also elevated substantially, 21.41%, going from 509 in Might to 618 in June. In Kendall County, foreclosure filings jumped from 143 in May possibly to 165 in June accounting for over a 15% boost in filings.

Foreclosure filings for June 2012 have also improved from last year when in June 2011 foreclosure filings had been at only six,032. Comparing June 2011 to June 2012, there was a small over a ten% enhance in foreclosure activity in June of this year. The 3 counties with the all round highest increases in the quantity of foreclosures filed from June 2011 to June 2012 were McHenry, Kendall, and Lake. McHenry county had the biggest boost going from 224 foreclosures in June 2011 and improved over 50% to 336 filings in June of 2012. Kendall had the second largest improve from 117 foreclosures in June 2011 and jumped to 165, almost a 30% improve. Lake county had the third biggest boost went from 446 foreclosure filings final June and improved 27.eight% to 618 in June 2012.

An increase in foreclosure filings was unfortunately expected. The foreclosure approach was slowed down, and in numerous situations stalled fully, since late 2010 simply because of numerous federal and state investigations into fraudulent mortgage-servicing techniques that became typically known as the robo-signing scandal. The robo signing scandal was finally settled upon earlier this year. Simply because of this, servicers and lenders are just starting to go via the backlog of foreclosures to file foreclosures that should have currently been processed final year. As the distressed loans are becoming filtered via, theres a specific batch of those that are initially getting pushed via the foreclosure method: those that are not deemed a very good fit for a loan modification, do not qualify for government refinancing applications, or even short sales.