Minneapolis, Minnesota (PRWEB) January 05, 2013

The Minnesota Foreclosure Prevention Q3 report states, “There had been 4,451 foreclosures in Minnesota in Q3 of 2012, down 10 % from Q3 of 2011. Although Metro foreclosures (down 12%) saw a greater drop than Higher Minnesota (down 7%), the relative relief was widespread, with the prime 10 counties in foreclosure seeing declines, year-over-year”. Although declines in Minnesota house foreclosures reflect a statewide trend over 20011 – 2012, the number of foreclosed houses are nonetheless historically high, upwards of 300% higher than foreclosure totals in years prior to the housing crisis.

Lenders, who have frequently resisted erasing mortgage debt, are now forgiving millions of dollars in house loans. The distinction indicated in the Foreclosure Prevention Report has come from government incentives, political pressure, and a $ 25 billion settlement amongst 5 major lenders and 49 attorneys basic. “Property owners, feeling ‘stuck’ unable to sell their residence before they can get a new one, are properly locked out of the housing market. Five years into the housing recession, theyre also more likely to think about the drastic move of walking away from their mortgage, adding to shadow inventory,” says Jenna Thuening, owner of Property Location.

Highlights in the Minnesota Foreclosed Properties Q3 Report show powerful and steady progress

Twin Cities foreclosed residences in 2011 Q3 totaled 2,969

Twin Cities foreclosed houses in 2011 Q3 totaled 2,615

Twin Cities foreclosed houses down 11.9%

31 counties reported far more foreclosed residences and 58 counties showed fewer foreclosed homes

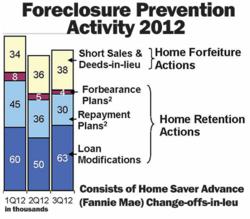

Encouraging news released January three by the Federal Housing Finance Agency (FHFA) that Fannie Mae and Freddie Mac completed much more than 134,000 foreclosure prevention actions in the third quarter of 2012.

Leading Points In TheFHFA Foreclosure Prevention Report:

1) Year-to-date, Fannie Mae and Freddie Mac have helped property owners by facilitating roughly 411,000 foreclosure prevention actions.

two) Almost 38,000 quick sales and deeds-in-lieu of foreclosure had been completed in Q3 of 2012, up 4 percent over Q2.

three) 45 percent of struggling residence borrowers who received loan modifications in the third quarter reduced their monthly payment by over 30 %.

four) Much more than a single-third of loan modifications completed in the third quarter integrated principal forbearance. NOTE: see explanation that principal forbearance is not the very same as principal reduction.

five) The number of the Enterprises delinquent borrowers has declined 9 % since the beginning of 2012.

six) REO inventory continued to decline as property dispositions outpaced house acquisitions in the course of the third quarter. An REO (Genuine Estate Owned) is a home that goes back to the mortgage firm right after an unsuccessful foreclosure auction and are typically in poor condition.

To help stabilize the housing industry, proponents of principal reduction argue that each home owners and lenders are far better off avoiding those defaults. The recent National Mortgage Settlement between 49 states, numerous federal agencies and 5 big banks is hoping to market the practice by providing those lenders with incentives to reduce loan balances, says Thuening. Home Location sees the following techniques foreclosure prevention actions effect home owners:

House Forfeiture Actions

1) Brief Sales

two) Deeds-In-Lieu of Foreclosure

Home Retention Actions

1) Forbearance Plans

two) Repayment Plans

3) Loan Modifications

Calculated Threat explains what this term ‘principal forbearance’ actually means. What the FDIC apparently implies by ‘principal forbearance’ is not what most men and women think they mean by ‘principal reduction’. Nonetheless, with the principal, what the FDIC is performing is not forgiving principal but providing an interest-totally free forbearance of repayment of part of the principal. This indicates that the actual principal amount due and payable at maturity of the loan (or sale of the home) is the original unmodified principal quantity, much less any and all periodic principal payments the borrower makes until maturity or sale.

Quick sales and deeds-in-lieu spare the home owners from the foreclosure method. Even so, they still have to leave their properties and that is traumatic for the homeowner. “The preferred outcome is to preserve property owners in their houses, if attainable, with a permanent principal reduction. Housing and Urban Development (HUD) Secretary Shaun Donovan mentioned his agency wants to encourage much more principal write-downs to keep people in their properties, even when those loans are backed by Fannie Mae and Freddie Mac,” according to a report in The Hill posted on March 4, 2012 titled Dems Raise Pressure on Fannie, Freddie Regulator to Create-down Mortgages. The Foreclosure Prevention Report for 2012 shows the dedicated efforts of Fannie Mae and Freddie Mac to that finish.

Twin Cities homeowners may possibly get in touch with 612-396-7832 and ask for Property Destination’s assist to quit foreclosure and enjoy staying in your house.