Minneapolis, Minnesota (PRWEB) December ten, 2012

November Housing’s Scorecard announced that 1.3 million homeowner assistance actions have taken spot through the Producing House Reasonably priced Program, assisting to absorb shadow inventory.

House Destination’s owner Jenna Thuening, says, “Housing analysts have the dodging process of predicting the emergence of shadow inventory, the catalog of homes on the edge of foreclosure or in the beginning stages, destined to be purchased by the banks and then re-marketed to property purchasers and investors”. RealtyTrac reports foreclosure sales improved in the third quarter of 2012 and housing nevertheless has over five,300,000 mortgages in the foreclosure pipeline.

White Property Scorecard gains that lessen foreclosure dangers incorporate:

More than 1.1 million home owners have received a permanent modification via HAMP, getting lowered very first lien mortgage payments by a median of about $ 542 every single month more than 1-third of their median prior to-modification payment saving a total estimated $ 16.2 billion in monthly mortgage payments.

Practically 100,000 second lien modifications started through the Second Lien Modification Plan, and more than 80,000 home owners exited their properties by means of a brief sale or deed-in-lieu of foreclosure with assistance from HAFA.

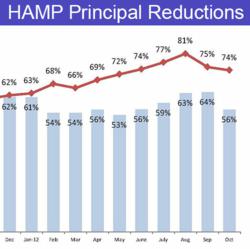

Property owners at the moment in HAMP permanent modifications with some form of principal reduction have received approximately $ eight billion in principal reduction.

Permanent modifications assisting property owners avert foreclosure function the following modification steps:

97.1% function interest price reductions

60.9% provide term extension

32.% incorporate principal forbearance

“The Administration remains focused on continuing to boost requirements for the mortgage sector to aid families keep away from foreclosure,” stated Treasury Assistant Secretary for Monetary Stability Tim Massad. “We continue to push the industry to provide much better service to property owners even though expanding the variety of solutions offered to households facing mortgage concerns.”

Goldman Sachs offers 3 causes why delinquent residences never always translate into foreclosure liquidation and turn into shadow inventory.

1) Delinquency History’s Differ For the duration of Foreclosure Timeline

Lender Processing Solutions (LPS) data show that 40 percent of foreclosure begins filed in current months consist of “recycled or repeat foreclosures” versus “new foreclosures”. More than half of the monthly transitions from being existing to getting 30-day delinquent are from mortgages that have delinquency history during the previous 12 months, causing a variance in month to month reporting.

2) Lender Service Responses Differ

Transitions in between different overall performance states are heavily dependent on government policies, exactly where it is left to the state, and lender and servicer responses to government policies. For example, transitions from getting delinquent to being existing will enhance when a lot more loan modifications are implemented. Conversely, transitions from getting present to being delinquent will decline when refinancing qualification aren’t gripped so tightly.

three) A lot of In Process Foreclosure Are Averted

Not all foreclosure filings are foreclosure completions. Even prior to the robo-signing scandal surfaced and the foreclosure moratorium took effect, a mortgage was as probably to pull out of foreclosure status due to homeowner’s taking action and managing to acquire a loan modification, or other forms of assist.

If homeowners’ mortgage tax exemption expires as we face the pending fiscal cliff, it could slow the $ 25 billion National Mortgage Foreclosure Settlement that five national lenders struck with 49 states and the federal government in March. That deal requires banks to use the bulk of the penalties for borrower help, such as at least $ ten billion in principal reduction, required to maintain pre-foreclosures and shadow inventory down.

“The Minneapolis housing market absorbed shadow inventories by means of modifications helping several home owners stay away from foreclosure. Distressed properties are plagued by extra weights to their default status or their underwater adverse equity status. They additionally add concern due to their frequent state of disrepair. Also often they turn out to be the blight of otherwise exceptional true estate neighborhoods, potentially effecting house values,” commented Thuening.

According to BusinessWeek, Peter Coy says, “These are the most dangerous assets in the huge shadow inventory portfolio of properties. Most banks have not put these wrecked houses on the market for a variety of factors, or at least not but. There is no query that many genuine estate investors and flippers would adore to obtain these residences, but in performing so they will manage to depress the cost recovery currently underway.”

The housing marketplace remains fragile to a certain degree. While it is the bright spot in the economy, the housing recovery is extremely dependent on other macroeconomic aspects such as unemployment, builder optimism, and consumer optimism. These variables, which the housing market place depends on to thrive, are subject to volatility. A considerable quantity of properties in the shadow inventory come on the industry at the identical time, deep periods of unemployment or widespread low consumer optimism, could reverse progress in lowering shadow inventory.

Minneapolis area house purchasers looking for to acquire pre-foreclosure residences, or facing foreclosure may possibly reach Home Location by calling 612-396-7832.