New Hyde Park, NY (PRWEB) January 19, 2011

Data revealed by ForeclosureListings.com confirms that jobs and economic stability reflect the overall temperament of the citizens. While some cities and states languish due to insufficient jobs and income, other areas show a more sustainable economic base, with or without the well intended plans of the government to help people keep their homes.

Government moratoriums over the past few years have had very little effect on the volume of foreclosure postings filed during 2010. 2.39 million home foreclosures were initiated during the first 11 months of 2010, and 1.01 mortgaged homes were completely executed during that time. In fact, it has been said by researchers and loan modification companies that the governments plans to relieve some of the hardships so many Americans are experiencing, that much of the money secured with the government was not and has not been released to those most in need of it.

Foreclosure sales dropped sharply in October and November of 2010, as several large lenders suspended foreclosure proceedings in the wake of the quick, robo-signing scandal. Lending institutions were ramrodding paperwork through without performing the due diligence necessary to ensure that all information was proper and accurate, which often times were not, resulting in some homeowners being removed unnecessarily or illegally from their homes, and damaging their credit.

According to recent figures, foreclosure sales plummeted from nearly 120,000 in September to 69,000 in October and 55,000 in November, as the foreclosure process slowed or suspended temporarily as lenders rechecked their information and policed their procedures.

During this time, foreclosure starts declined from nearly 250,000 in September to 205,000 in October, but then picked back up again to 221,000 in November.

The glut of bank-owned properties has helped contribute to sharply declining house prices in many areas of the country. Bank owned properties are ready to be sold; they are vacant and the bank is motivated to find a buyer. The number of short-sale listings increased to nearly 55 percent, as banks were anxious to remove bad debts from their books and get what they could as soon as they could.

While unemployment is directly tied to these bleak housing trends, tens of millions of Americans are worried about their home values. Almost 30 percent of homeowners with mortgages are underwater, meaning that they owe more than their home is worth on the market. Even more people worry about their ability to pay their mortgages. Home prices could continue to adjust downward while a cloud of uncertainty keeps the home-buying market uneasy and unwilling to commit to a mortgage commitment.

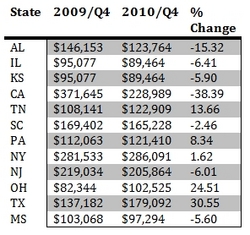

ForeclosureListings.com data for the fourth quarter of 2010 compared to the same period a year earlier reveals that in some states the foreclosure market has improved and in others, where unemployment and under employment has manifested, it has worsened.

###

Find More Loan Modification Press Releases