Discovery Bay, CA (PRWEB) January 14, 2009

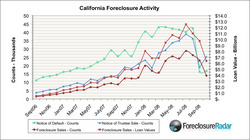

ForeclosureRadar, the only website that tracks every California foreclosure with daily auction updates, these days issued its California Foreclosure Report for December 2008 and year-finish summary. Notices of Default have rebounded from the stall brought on by California State Senate Bill 1137, which temporarily slowed foreclosures by imposing new specifications on lenders. With 42,421 filings in December, Notices of Default are back to the record levels reached in the second quarter of 2008, almost doubling the 21,557 Notices of Default recorded in November. Notice of Trustee Sale filings have been comparatively flat month-more than-month, even so Notices of Trustee Sale are filed an typical 116 days following the Notice of Default so a rebound in the coming months is most likely.

California saw unprecedented foreclosure activity in 2008, with 249,940 properties sold at trustee sale auction – representing $ 107.eight Billion in combined loan value. Of those properties 96.4% went back to the lender soon after no bid was received from a third-celebration.

Higher-level findings for 2008 include:

There have been a total of 437,955 Notices of Default filed in 2008, an enhance of 56 percent more than the 279,821 Notices of Default filed in 2007.

Notice of Trustee Sale filings improved 122.9 % more than 2007 rising from 157,273 filings in 2007 to 350,514 filings in 2008. Of the Notices of Trustee Sale filed in 2008, 16 % remain scheduled for sale at auction, 17 % have been cancelled, and 66 % have been sold at auction.

Properties sold at auction increased by 158 percent by volume, and 179 percent by combined loan value. Lenders took back a total of 241,093 properties, with a combined loan worth of $ 103.9 Billion.

The amount lenders discounted properties at auction from the outstanding balance elevated from an average discount of 16.1 % in January to 39.5 % in December. In January only three percent of properties taken to auction had been deeply discounted (bidding began at a discount of 50 percent or much more from the loan balance). By December 40 percent of sales had been deeply discounted.

The time among the filing of a Notice of Default, and a home getting sold at auction on the courthouse actions increased 19 days over the course of the year, to an average of 165 days in December.

Higher-level findings for December contain:

Notices of Default increased one hundred percent over Notices recorded for November, to a total of 42,421 default filings, a 24.7 percent enhance more than December 2007.

Notices of Trustee Sale, which set the auction date, time and location, had been flat from November to December, with 27,497 filings. Notices of Trustee Sale for December represent a 29.eight percent year-over-year boost, but are nonetheless 30 percent below the peak levels reached in July of 2008.

Properties taken to sale at auction enhanced only slightly between November and December, to 16,298 sales, a 72.6 % enhance from the exact same time final year. Third party purchases at trustee sale auction decreased 12.5 % from November 2008, but have been nevertheless 156 percent above third party purchases in December 2007. Lenders took back almost 95 % of the 16,298 properties sold at auction, with a combined loan value of $ 8.95 Billion.

“The work by the California State Legislature to lessen foreclosures has now clearly failed,” says Sean O’Toole, founder of ForeclosureRadar. “While State Senate Bill 1137 was well intentioned, forcing lenders to talk to property owners will not repair this difficulty.”

Even though a quantity of lenders have announced considerable loan modification applications to decrease payments to cost-effective levels, these plans fail to address the reality that the typical foreclosure in California now has $ 180,000 in damaging equity. “Lowering payments may possibly offer a short-term fix,” adds O’Toole, “but lenders just never have enough reserves to reduce principal balances adequate to help property owners in foreclosure escape the prison of debt their property now represents.”

In December, the typical estimated worth of a property sold at foreclosure auction was $ 283,624, with an average total loan balance of $ 464,270. Of these, 60 percent had second mortgages for which small or no equity remained to secure their interest in the house. By not foreclosing, second mortgage holders often retain their capability to collect on loans even after their secured interest is wiped out by the foreclosure of a initial mortgage. This problem frequently impairs the capability of very first mortgage lenders to modify their loan sufficiently to aid the homeowner, a basic truth that further curtails the effectiveness of SB1137.

CALIFORNIA FORECLOSURE REPORT METHODOLOGY

Rankings are based on population per foreclosure sale. NOD indicates the number of Notices of Default that have been filed at the county, and NTS indicates filed Notices of Trustee Sale. Sales indicates the number of properties sold at foreclosure auction. Percentage changes are primarily based on monthly Sales. The data presented by ForeclosureRadar is based on county records and person sales results from everyday foreclosure auctions all through the state – not estimates or projections.

ABOUT FORECLOSURERADAR.COM

ForeclosureRadar is the only net website that tracks each foreclosure in California with everyday updates on all foreclosure auctions. ForeclosureRadar functions unprecedented tools to search, manage, track and analyze preforeclosure, foreclosure auction, brief sale and bank owned real estate. The web web site was launched in May 2007 by Sean O’Toole, who spent 15 years building and launching software companies before getting into the foreclosure business in 2002 where he has effectively purchased and sold far more than 150 foreclosure properties. ForeclosureRadar is an indispensable resource for real estate agents, brokers, investors, lenders, mortgage brokers, attorneys and other true estate pros specializing in the California true estate market.

###